Tax exemption: How to reduce your tax liability

Tax exemptions provide financial relief for taxpayers. Yearly tax exemptions are interesting for employees because they reduce the monthly tax payable. Everyone who pays income tax - including entrepreneurs, the self-employed, retired people, and pensioners - benefits from tax exemptions. How high they are in the end depends on what you qualify for, how much you earn, whether you’re married, and how many dependents you have.

What is a tax exemption?

Americans welcome tax exemptions with open arms since it means they get to keep more of their wages and have to give less to the state and federal government.

A tax exemption is money that the Internal Revenue Service (IRS) allows taxpayers to subtract from their annual taxable income, expressed on their tax reform. The more exemptions you’re able to take, the more you can lower your tax bill.

Tax deductions and tax credits are types of tax exemptions since they also enable you to save money on your taxes. However, they do slightly differ from one another:

- Tax exemption: Enables you to curb your tax bill based on your tax-filing status and the number of dependents.

- Tax deduction: Is for items that you can deduct on your tax form on an ongoing basis over the whole year. Examples include traveling, home office accessories, and interest on student loans.

- Tax credit: Is a sum of money that can be offset against a tax liability, on a dollar-to-dollar reduction basis. Once the total tax obligation has been determined, you can subtract the dollar value of any tax credits allowed.

No matter which tax exemption you use, how much you save on that tax exemption is up to you. The more exemptions you can correctly claim, the more you will save on your federal or state tax bill.

Different types of tax exemptions

The most common forms of tax exemption are personal exemptions, dependent exemptions, tax-exempt organizations, and state and local tax exemptions. Below is an introduction to each type.

Personal exemptions

For tax years prior to 2018, every taxpayer is entitled to one exemption and if you’re married and file your taxes together, your spouse also gets an exemption, which you can file on the same tax form.

You are only allowed to claim a tax exemption for yourself if another taxpayer doesn’t have you named as a dependent. Spouses aren’t classified as being dependents of each other, but it is still possible to claim the exemption for each spouse on a couple’s tax return.

Dependent exemptions

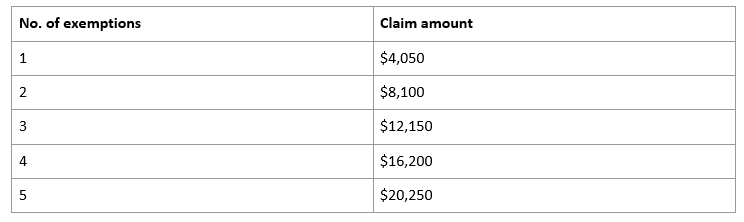

You’re allowed a single exemption for each individual classed as a dependent. This is possible even if the dependent files their own tax return in the same year. It’s usual for taxpayers to take an additional exemption for each child or family member as long as they have resided in the taxpayer’s home for half the year or are under the age of 19 (or 24 if a full-time student) in the year that you claim the tax credit. Some relatives can also qualify if they live with you, as well as your parents even if you don’t reside together. In 2017, this is the amount you could claim when taking a dependent tax exemption:

This table refers to 2017 since starting in the 2018 tax year, personal exemptions have been suspended until 2025. More information on this is mentioned below.

Tax-exempt organizations

The IRS allows some organizations to claim tax-exempt status. These are mainly non-profit groups or religious groups, but can also be social clubs and trade associations. The general rule of thumb is that if your group serves the public, the IRS provides a massive tax break to make it easier for these groups to promote their causes. These groups are exempt from paying federal taxes, and those that run the groups get their own tax deduction. Federal laws don’t always work in the same way as federal laws though so it makes sense to research first to see if your group is exempt from federal AND state laws or just one of them.

State and local tax exemptions

In addition federal tax exemptions, taxpayers can also claim state and local tax exemption. Sometimes businesses are exempt from taxes if they are located in a low-income area. The hope is that more businesses are attracted to the community. Another example is consumers often get a tax exemption on sales tax for a specific period of time (these are referred to as “tax holidays”).

Personal exemptions suspended by tax reform

In December 2017, Congress passed the largest tax reform bill in over 30 years. A part of the Tax Cuts and Jobs Act states that the $4,050 personal exemption is being temporarily eliminated, meaning that families with a lot of dependents will likely end up with a higher tax bill. Personal exemption wasn’t able to be fully scrapped, which is why it will be suspended from 2018 until 2025 unless it is extended by Congress.

How to claim tax exemptions

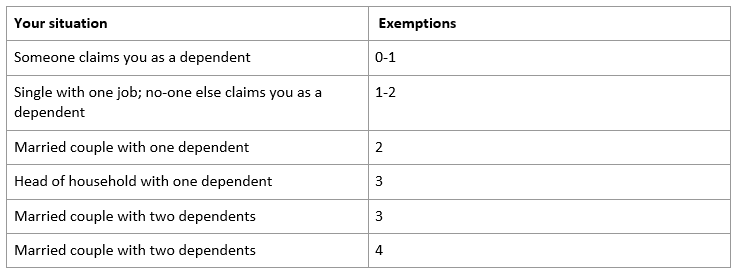

The IRS has a personal allowances worksheet to help you work out how many tax allowances you should claim. This is for your own personal use; you don’t need to submit it to anyone. Here are the general guidelines of how many allowances you can claim:

If you work more than one job, you still have the same number of allowances, but you have to simply split them across all jobs.

You claim exemptions when you file your annual return by using IRS Form 1040. To calculate the amount, you multiply your total claimed exemptions by the IRS-specified dollar amount for the current tax year, and then deduct that amount from your taxable income. The exemptions that you’re able to claim on your tax return will help you work out how many allowances to claim when submitting Form W-4 to your employer (W-4 is the form that every employee needs to complete when starting a new job). By claiming the correct number of allowances on the form, the amount deducted from payroll should adequately cover your annual tax liability. The form has instructions to make it easier to complete correctly.

Tax credits that survived the 2018 tax reform

Since there are no more personal exemptions allowed between 2018 and 2025 (possibly longer), there are some tax credits you can claim to help lower your tax amount.

Head of Household Filing Status

In order to qualify for this, you must have a dependent. This status entitles you to a larger standard deduction than if you just filed a single return. As of 2018, you would receive $18,000 deduction instead of $12,000 just by claiming this one dependent. It also means you can earn more before having to change to a higher tax bracket. You must, however, be considered unmarried to file as head of household, which means either being single, or not having lived with your spouse for the last six months.

Child Tax Credit

Naturally you need a child to qualify for this credit and they need to have their own Social Security number. This credit was luckily not eliminated by the Tax Cuts and Jobs Act (TCJA) and was even increased from $1,000 per child in 2017 to $2,000 per child in 2018. Due to the credit being partially refundable, you can receive up to $1,400 more in your tax refund if there is any credit left over after you’ve erased your tax debt.

The Child and Dependent Care Credit

The TCJA has also kept the Child and Dependent Care credit, which is a credit equal to 20% to 35% of what you spend on childcare, helping you to go to work or look for work. The percentage depends on how much you earn as well as how many children (under 13 years old) you have, but for each child dependent you can expect up to $3,000 in care costs. If you are married, your spouse must be unavailable to care for your kids because they are working, are disabled, or are a full-time student.

The Earned Income Tax Credit

You don’t actually need a child dependent to claim this credit although you would get more money back. The aim of this credit is to give money back to lower income families, and it’s also refundable. If you don’t have a child dependent, you will still qualify for this credit as long as your income isn’t more than $15,270 for the year if you aren’t filing a joint married return. If you are filing together with your spouse, then you can earn up to $20,950 and still qualify. $519 is the maximum credit you would be entitled to if you don’t have a dependent, but, for example, if you have three child dependents (no older than 19 years, or 24 years if they are still studying), your maximum credit would be $6,431.

Education Tax Credits

The Lifetime Learning Credit or the American Opportunity Credit also survived TCJA’s wrath. You can only claim one or the other though, and you can also claim them for your spouse or your dependents. For the latter credit, the student must be in the first four years of college to qualify, but the Lifetime Learning Credit isn’t as restrictive. The maximum AOC per student is $2,500 and the maximum LLC is $2,000, which is equal to 20% of the first $10,000 you pay in tuition and fees each year.

Tax deductions for your dependents

Your dependents can also play a role in helping you qualify for tax deductions. The student loan interest deduction is worth up to $2,500 in interest you paid on student loans over the year, be it for yourself, your spouse, or your dependents.

The tuition and fees deduction for post-secondary education is also an option, although its status is still up in the air for 2018 since it wasn’t revived by the TCJA.

Click here for important legal disclaimers.