How to book capital contributions and withdrawals correctly

During a business owner’s everyday life it is commonplace for money to be transferred from the company to their account for private purposes, or for the business owner to inject their own money into the company. This process is known as capital contributions and withdrawals. For sole proprietors and partnerships, these financial transactions are not a major problem – if they are correctly recorded. Otherwise, there is a significant risk of conflict with the IRS and state tax offices.

Capital contributions and withdrawals: How to book them properly.

Two things are important when it comes to recording the booking of a capital contribution or withdrawal:

- The value of the contributions or withdrawal

- To which accounts you have paid or withdrawn the money

It is important for both, whether a private withdrawal or deposit is taking place.

More information on values and types can be found in our respective articles on capital contributions and withdrawals.

To be able to record the booking correctly, you will need at least one private account in your company’s chart of accounts. If there are several individuals in the company who are allowed to make transactions between personal and corporate assets, several private accounts are generally available. These are sub-accounts under equity. In practice, many companies use their own account for private withdrawal and private contributions.

When it comes to private withdrawals, you book the amount from Private to Cashier (or any other corresponding account) and to the Private Deposit from Cashier to Private. When you close a private account, withdrawals appear on the left (debit) and deposits on the right (credit).

In the company’s balance sheet, private accounts are included in the equity account. Depending on the ratio of picking to deposit, write the sum of private accounts either to the left side (more picking than deposit) or to the right side (more deposit than picking). The private accounts are therefore either a burden or relief on equity. Profit and loss are included as further equity sub-accounts.

Booking rates: Private contributions and private withdrawals – including examples

In order to understand the correct booking rates, we will go through using different contributions and withdrawal methods, each with suitable examples. So, let’s first take a look at the simplest, most common form:

Booking cash contributions and cash withdrawals

When it comes to cash contributions or withdrawals, you transfer money (either in cash or by bank transfer) between your own assets and that of the company. In addition to a private account, you also need an account cashier or bank. In this case, let’s assume that you first take the money out of the cash register and pay a different amount of money back at another time.

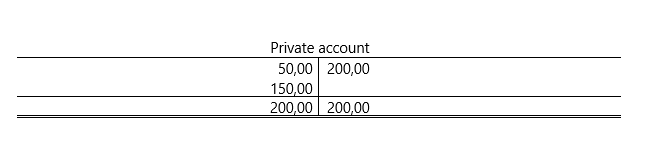

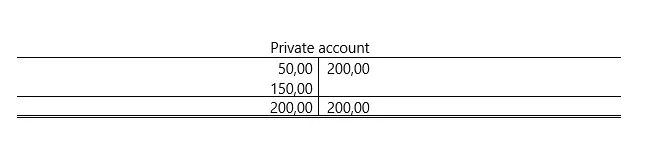

First, you take 50 dollars from your company’s cash register:

Private withdrawal (1800) $50.00 from the cash register (1000) $50.00

Then you put 200 dollars back into the cash register:

Cash register (1000) $200.00 as a private deposit (1890) $200.00

If the private accounts were to be closed, it would look like this:

The debit column must be filled with a balance of 150 dollars to complete the account. This is finally included as a credit in the balance sheet account equity:

Booking a non-cash withdrawal

Now, let’s imagine that you’re making a withdrawal in kind by taking a product from the company for private use. To do this, you do not set the production or acquisition value, but the normal list price, i.e. the price that you would also charge a customer – including sales tax (if applicable). You must register it separately in a corresponding account. For simplicity’s sake, let’s say the net price of a chair is 119 dollars.

- A withdrawal by the entrepreneur for purposes outside the enterprise (goods) $100

- And sales tax at 19% $19.00

You end up closing the private account and the equity account the same way as in the first example.

Book usage withdrawal

If you don’t remove an item completely from the company, and instead just use it privately, you must book a usage withdrawal (and also tax this amount as a monetary advantage). This is particularly interesting for the private use of the company car. Here, too, you calculate the partial value in principle: To what extent is the vehicle used privately?

To determine the partial usage value, you can keep a driver’s logbook. Alternatively, you can use the fleet average valuation rule (FAVR). You simply add 1% of the US net list price for the vehicle per month – including optional equipment and whether the car was purchased second hand. The business owner can enjoy a flat rate discount of 20% on pre-tax car related costs, but sales tax is payable on anything else. The FAVR is only applicable to cars valued at less than $50,000 as of 2018.

Let’s say you have a company car with a fleet average valuation of $50,000. One percent of this is 500 dollars. Of this, twenty percent is $100. Let’s say you live in a state with sales tax: it will only be payable for $400, $100 less than the total amount. Let’s say the sales tax rate is 19 percent: total sales tax will amount to $76. The private withdrawal for the month in question is therefore $576. You should post this amount to the account free of charge value levies.

The FAVR may only be applied if the vehicles in question are used for operational purposes at least 50 percent of the time. If you are unsure of how to measure this, please consult a tax professional for advice.

Free levies $576,00

- Use of goods for purposes outside the company: $400

- Sales tax at 19 %: $76.00 and

- Use of goods for purposes outside the company without sales tax (personal car use): $100

Booking a private contribution

In our final example, let’s look at private contributions and their bookings. Let’s say you bought a PC a year ago that was primarily used by your child. However, they have now moved away to college and just use their laptop. You want to hand over the PC to your company. You specify the amortized acquisition cost as a partial value.

You originally paid $1,200 for the PC. The computer has subsequently depreciated and now has a value of $800 after one year (we assume in the example that the deposit takes place exactly one year after purchase). With this value provided, the PC now appears in the records.

Other operating and business equipment $800.00 in Private deposits $800.00

These are only selected, simply examples. In reality, each situation must be considered individually.

Click here for important legal disclaimers